Assessing Returns for Stocks In Watchlists

A watchlist is a collection of stocks that can help you identify

stock market trends by revealing securities driving those trends. In addition, you can also think of a collection

of watchlists as sets of stocks designed to reflect changing growth rates in complementary

market areas.

It is not unusual for traders to take advantage of multiple

contrasting watchlists. A watchlist does

not necessarily contain your current portfolio of holdings. Instead, you can use a set of watchlists to

identify stocks that are currently good candidates for either adding or

removing positions from your current holdings.

Trading decisions about when to buy, hold, or sell securities can be

based on watchlists as well as technical and fundamental indicators along with

trading narratives.

Watchlists can be especially important for swing traders who

hold positions over several weeks or months, and then exit positions within

days when expectations are not fulfilled or much better opportunities manifest

themselves. In contrast, entries within

a watchlist as well as the number of watchlists tracked can update at a much

slower pace. You can grow a collection

of watchlists over several years – keeping some unchanged, revising others

quarterly, and adding new ones as market actions dictate.

This post gives an example of constructing and tracking a collection

of watchlists with leaders for several different areas. The watchlists are compiled based on data

collected during 2024. It is my hope

that you find the criteria and steps used for constructing watchlists in this

post helpful when you are constructing your own watchlists that reflect your

personal investment style. The

Concluding Comment section at the end of this post offers some use cases for

different kinds of investors for the analyses presented in this post.

Stocks Tracked in This Post

There are many criteria that you can use for selecting

tickers for a watchlist. The steps

followed for this post started with an identification of leading areas for

securities in 2024 as well as prior analyses from earlier posts to this blog.

While tracking returns from securities, you will typically

find it of value to use a benchmark. The

SPY ETF (exchange traded fund) is a good benchmark for growth rates because its

performance reflects the stocks in the S&P 500 index. Only top performing tickers can match or

exceed this index. When a trader

composes a watchlist of tickers beating the SPY, then the watchlist tickers have

an excellent chance of delivering outstanding growth rates to the trader’s

account balance.

The following table itemizes the four watchlists along with

the SPY benchmark ticker tracked during 2024 in this post.

- The SPY ticker is the benchmark for assessing the growth rates of all other tickers.

- Tickers for the second watchlist category are ETFs for four major market indexes. Each of the major market indexes are leveraged so they target three times the daily performance of their underlying index. The SPY benchmark ticker is an unleveraged ticker for the S&P 500 index.

- The Crypto watchlist category is comprised of six tickers for securities that participate in the cryptocurrency market.

- HUT and WULF are for bitcoin miners.

- GBTC is a well-known ETF whose price fluctuates with the daily return of bitcoins relative to US dollars.

- BITX is an ETF that targets a daily return of twice the value of bitcoins relative to US dollars.

- MSTR is the ticker for a company that acts as a treasury for bitcoins. The company is among the top corporate holders of bitcoins with a count of over 400,000 bitcoins as of the time this post is published.

- COIN is the ticker for a publicly traded cryptocurrency exchange (Coinbase).

- The Semis and AI watchlist category has three types of tickers.

- PLTR and BBAI denote publicly held companies that specialize in the delivery of solutions with built-in artificial intelligence.

- NVDA is the leading vendor for chips to run generative AI solutions. Other hardware vendors that participate in implementing generative AI solutions include these tickers: TSM, ARM, and AVGO.

- The USD ticker symbol is for the ProShares Ultra Semiconductors ETF. The ETF relies on the Dow Jones Semiconductor index. Some of the participant firms in this index provide chips for generative AI solutions.

- The ETFs Launched in Last 3 Years watchlist is comprised of ETFs launched in the last three years as of December 2024.

- The PTIR, MSTU, NVDX, TSLL, FBL tickers denote single-stock ETFs. For example, PTIR is for the PLTR ticker, and MSTU is for the MSTR ticker. All five of these tickers have a leverage of two times the daily performance of their underlying security.

- The IBIT ticker is for the largest bitcoin ETF in terms of assets under management.

Downloading Data for Analysis

This post section illustrates how to download from Google Finance weekly historical

close prices from 2024 for the tickers itemized in the previous section. The GOOGLEFINANCE function pulls the downloaded

data from Google Finance to Google Sheets.

Self-directed traders and securities analysts can get started using

Google Sheets without charge so long as you have a Google account, such as for

Gmail.

A pair of prior posts (“GOOLEFINANCE

Function in Google Sheets Can Download Historical Data via CSV Files”

and “Do

Returns from the GOOGLEFINANCE Function In Google Sheets Match Returns from

Yahoo Finance?”) describe and present examples of how to download daily

historical close from Google Finance via the

GOOGLEFINANCE function. This post section extends the prior posts with

examples for downloading weekly historical close values.

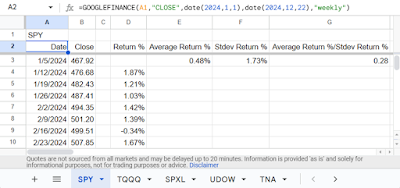

The following excerpt from Google Sheets downloads weekly close

prices from the Google Finance site with the GOOGLEFINANCE function for the SPY

ticker. The instance of the

GOOGLEFINANCE expression within cell A2 in the following screen shot takes five

parameters.

- The first parameter is a cell address (A1). This cell address contains the ticker (SPY) for which to return weekly historical data.

- The second parameter names the type of data to return – which are close prices in this example.

- The third, fourth, and fifth parameters indicate the start and end dates for which to return weekly close prices.

- The start date – indicated by date(2024, 1,1) – is the first possible date for which data is collected. Because markets are closed on January 1, data collection does not start until Tuesday, January 2, 2024.

- The end date – indicated by date(2024, 12, 22) – is the last possible date for which data are collected for this post. Because markets are closed on weekend dates (January 21 and 22), the last date for which weekly close prices are returned by the GOOGLEFINANCE expression is Friday, December 20, 2024.

- The value of “weekly” for the fifth parameter indicates close prices should be returned on a weekly basis.

- As a result of these parameter values, the function populates weekly closing dates and prices on Fridays from January 5, 2024 through December 20, 2024.

The following screenshot displays the first several rows

returned by the GOOGLEFINANCE function in cells A3 through B10. The data appearing in columns D through G is

derived by functions for data in column B.

The functions are critical to assessing how well tickers are performing

in your watchlists.

Tickers that do especially poorly relative to other tickers can be dropped and replaced by other tickers. All of the tickers within this post may be worthy of inclusion in the watchlists of many traders, but there are a few tickers that are especially worthy or inclusion in your watchlists. These tickers will be highlighted in the “Sorted Performance Ranks Across Watchlists” and “Concluding Comments” sections.

The next screenshot shows an image from another sheet in the Google Sheets workbook named Watchlist from 2024. A Google Sheets workbook denotes a file with separate sheets for different, but related, datasets in different tabs within the same workbook.

As you can see from the preceding screenshot, the SPY tab

contains data for the SPY ticker. Also, the

preceding screenshot shows four other tabs are named for the tickers in the

Major Markets watchlist. To the right of

the tab named TNA, you can see arrowheads (< and >).

- The arrowhead pointing to the right allows the display additional sets of tabs for different tickers.

- You can successively press the arrowhead pointing to the right to discover additional tabs that are populated with data.

- At this point (or before), you can press the left arrow to return to a previously viewed set of tabs.

The following screenshot displays the second tab in the

initial set of tabs within the Watchlist from 2024 Google Sheets Workbook. This second tab differs most significantly from

its preceding tab because it contains TQQQ in cell A1 instead of SPY. The expression in cell A2 on the TQQQ tab is

the same as the expression in cell A2 on the SPY tab. Consequently, the TQQQ tab displays weekly

dates and corresponding historical close values for the TQQQ ticker.

The third, fourth, and fifth tabs in the preceding screenshot are named SPXL, UDOW, and TNA. The A1 cell value for each of these tabs is, respectively, SPXL, UDOW, and TNA. Consequently, the tabs display, respectively, weekly dates and corresponding historical close values for the SPXL, UDOW, and TNA tickers.

The completed version of the Watchlist from 2024 Google

Sheets Workbook contains a separate Google sheet for each of the tickers listed

in the “Stocks Tracked in This Post” section.

Analyzing the Downloaded Data for the Watchlist tickers

After downloading the weekly close prices for tickers into the

tabs of a Google Sheets workbook, the next set of steps are to

- compute the weekly percentage change in close prices between contiguous weeks for each ticker’s close prices,

- compute the average and sample standard deviation of the weekly percentage change values for each ticker, and

- across all tickers, compute the weekly average percentage change across weeks divided by the sample standard deviation of the weekly percentage changes for each ticker in all tabs.

These steps compute both the central tendency of the weekly percentage

changes in close prices and the weekly variation (as measured by the standard

deviation of the weekly percentage changes) in close prices for each of the tickers. Column D from the tab for each ticker displays

the percentage change between weekly close prices. Because you need two periods to compute

weekly changes, this metric is not available until the end of the second period

in a ticker’s dataset.

It is common to evaluate a ticker’s performance by dividing the

final close price by the initial open price.

However, this approach obscures the changes between periods. Even if there is a substantial change in

overall performance, this approach does not necessarily reflect the impact of successive

weekly changes up or down between the initial open price and the final close price.

Multiple successive weekly price declines may motivate a trader

or investor to sell a security even when its overall performance increases

substantially during a timeframe, such as a quarter or a year. By

selling on intermediate poor performance, a trader or investor can miss out on

the overall gain between the first and last weekly period. While there are many technical analysis tools

to help assess when to sell a security in the face of declining prices, none of

these tools are infallible regarding future growth over a timeframe, such as a

quarter or a year. By dividing the average

of the inter-period changes across weeks by the standard deviation of the

inter-period changes, you can at least compute an adjusted performance that

reflects inter-period variation.

Columns E and F in row 3 of the tab for a ticker display inputs

for computing the adjusted performance that reflects inter-period variation.

- The value in row 3 of column E reflects the average function output for the weekly close price percentage changes in column D. This value is the unadjusted weekly percentage price change.

- The value in row 3 of column F reflects the standard deviation function output for the weekly close price percentage changes in column D.

The value in row 3 of column G is computed as the ratio of the

value in row 3 of column E divided by the value in row 3 of column F. This ratio is the adjusted average inter-period

percentage price change for the weekly close prices on a tab.

Here are the resulting tables with the metrics discussed

above for the Major Markets watchlist tickers plus the SPY benchmark ticker. The first table shows the results sorted by average

return percentage of the weekly change. The

second table shows the results sorted by adjusted return percentage, which is

the average return percentage divided by the sample standard deviation of the

weekly return percentages.

- All the Major Market tickers have larger average return percentage values than the average percentage value for the SPY benchmark ticker.

- The SPY benchmark ticker has a higher adjusted return percentage value than any of the Major Market tickers. This is the result of the Major Market tickers all having larger sample standard deviation values than the SPY benchmark ticker.

- For traders and investors who can tolerate high dispersion for the average weekly percentage changes, any of the Major Market tickers will be a more lucrative choice than the SPY benchmark ticker. In contrast, the SPY benchmark ticker is a better choice for traders who will let themselves sell during a temporary decline over several weeks (because they do not believe in the potential of a higher, offsetting series of gains is likely to reverse the decline).

Here are the resulting tables with the metrics discussed above for the Crypto watchlist plus the SPY benchmark ticker.

- The SPY benchmark ticker has a smaller weekly average percentage change than any of the Crypto watchlist tickers.

- For the Crypto watchlist, the MSTR ticker has the first place rank no matter whether ticker ranking is by average percentage change or adjusted average percentage change. On the other hand, the SPY benchmark ticker nearly matches MSTR ticker performance when ranking tickers by adjusted average percentage.

- For all other Crypto watchlist tickers, the SPY benchmark ticker substantially outperforms all other Crypto watchlist tickers on adjusted average percentage change.

Here are the resulting tables with the metrics discussed

above for the Semis & AI watchlist plus the SPY benchmark ticker.

- The PLTR ticker ranks in first place for performance whether ranking the tickers is by average return percentage or adjusted average return percentage.

- The NVDA ticker improves its performance ranking from fourth place to second place when ranked by adjusted average return percentage instead of unadjusted average return percentage.

- Thirdly, the SPY benchmark ticker improves its rank from last place to third place when ranked by adjusted average return percentage instead of unadjusted average return percentage. This is a consequence of the SPY benchmark ticker having a much lower value for Stdev Price Change % than any of the Semis & AI watchlist tickers.

Here are the resulting tables with the metrics discussed

above for the ETFs Launched in Last 3 Years watchlist plus the SPY benchmark

ticker. This watchlist has six tickers

associated with it. As the watchlist

name implies all the tickers for the watchlist were introduced recently. In fact, two of the tickers have historical

performance for only 16 weeks (PTIR) or 14 weeks (MSTU), respectively. The other four tickers associated with the

watchlist have historical data over either 50 weeks (NVDX and IBIT) or 51 weeks

(TSLL and FBL).

- The first and second ranking tickers according to either sort order are PTIR and MSTU, respectively. The long-run significance of this outcome is somewhat questionable because these tickers have historical data for only around 15 weeks.

- The rank for the SPY benchmark ticker improves from last place to third place when ranked by adjusted average return percentage instead of unadjusted average return percentage. Again, this is because the SPY ticker has a lower dispersion relative to the other tickers in the watchlist.

Sorted Performance Ranking Within and Across Watchlists

Watchlists typically segment tickers based on one or more

criteria into different segments that are important to an investor or a trader. The watchlist names are

- Major Markers

- Crypto

- Semis & AI

- ETFs Launched in Last 3 Years

Other examples of watchlists include value stocks versus

growth stocks or small-cap, mid-cap, and large-cap stocks. While watchlists can be useful for

identifying rotations between watchlists over time, there are occasions when

traders want to identify the best (or the worst) ticker(s) regardless of the

watchlist to which they belong. This

section shows an example of how to perform that identification when ranking

performance based on unadjusted return percent or adjusted return percent.

There are a total of twenty-four tickers tracked in this

post.

The following table ranks the full set of tickers by unadjusted

return percent. The most important

observation are as follows.

- Tickers PTIR and MSTU rank in first and second place, respectively.

- The SPY benchmark ticker has a lower rank than any of the other tickers.

|

Sorted by Average Return % |

|||

|

Ticker |

Average Price Change % |

Stdev Price Change % |

Average Price Change %/Stdev Price Change % |

|

PTIR |

14.73% |

23.69% |

0.62 |

|

MSTU |

14.63% |

27.34% |

0.54 |

|

MSTR |

4.73% |

16.18% |

0.29 |

|

NVDX |

4.11% |

14.76% |

0.28 |

|

PLTR |

3.74% |

10.25% |

0.36 |

|

WULF |

3.61% |

15.57% |

0.23 |

|

TSLL |

3.12% |

18.42% |

0.17 |

|

BITX |

2.69% |

15.09% |

0.18 |

|

USD |

2.55% |

11.41% |

0.22 |

|

HUT |

2.50% |

15.01% |

0.17 |

|

BBAI |

2.48% |

19.19% |

0.13 |

|

NVDA |

2.28% |

7.11% |

0.32 |

|

ARM |

2.14% |

13.13% |

0.16 |

|

FBL |

2.01% |

10.12% |

0.20 |

|

COIN |

1.97% |

13.18% |

0.15 |

|

IBIT |

1.88% |

7.46% |

0.25 |

|

AVGO |

1.80% |

8.09% |

0.22 |

|

GBTC |

1.73% |

7.71% |

0.23 |

|

TSM |

1.54% |

5.90% |

0.26 |

|

TQQQ |

1.48% |

7.68% |

0.19 |

|

SPXL |

1.27% |

5.18% |

0.24 |

|

TNA |

0.77% |

8.69% |

0.09 |

|

UDOW |

0.68% |

4.68% |

0.15 |

|

SPY |

0.48% |

1.73% |

0.28 |

The next table ranks the full set of tickers by adjusted

return percent.

- Again, the PTIR and MSTU tickers rank in first and second place, respectively.

- For the unadjusted return percent ranking, the SPY benchmark moves from last place to sixth place. While SPY’s lower Stdev price percent value offsets the lower unadjusted return percent for most of the tickers, there are five tickers (PTIR, MSTU, PLTR, NVDA, and MSTR) that have sufficiently large unadjusted return percent values to overcome the SPY’s advantage for lower Stdev price percent value.

- In spite of the elevated rank for the SPY benchmark ticker when ranked on adjusted return percent, it is important to understand that low-dispersion securities sometimes come with lower unadjusted return percentages. As a trader or analyst, you are responsible for making the tradeoff between safety and total return value. Cchoose wisely because sometimes a safe smaller return may not be better than an unsafe and potentially larger return in the long-run.

Concluding Comments

This post tracked twenty-four tickers in four watchlists plus

the SPY benchmark ticker. The names of

the four watchlists are

- Major Market

- Crypto

- Semis & AI

- ETFs launched in last three years

The tracking of tickers was performed relative to two metrics.

- The first metric is the average percent return per week in the first fifty-one weeks of 2024. This metric is referred to as unadjusted return percent.

- The second metric is the unadjusted return percent divided by the standard deviation of the average weekly percent returns. This metric adjusts the unadjusted return percent by the dispersion in weekly return rates. The second metric is the adjusted return percent.

All the tickers tracked in this post are potentially

valuable for different types of investors/traders. Here are some suggestions for different kinds

of investors/traders.

- For traders/investors who are not averse to substantial weekly variation in unadjusted return percent, the top eight tickers based on unadjusted return percent are: PTIR, MSTU, MSTR, NVDX, PLTR, WULF, TSLL, and BITX. These tickers offer the highest unadjusted returns, but they also have the highest variability in weekly returns.

- For traders/investors who are extremely sensitive to weekly variation in unadjusted return percent, the SPY benchmark ticker has the lowest standard deviation for weekly return percentages, and it delivers a weekly unadjusted return percent of about .48 per week.

- For traders/investors who are willing to tolerate a little more variability in unadjusted weekly return percent, consider adding the UDOW and SPXL tickers to your portfolio.

- Finally, conservative traders/investors who seek even higher unadjusted return percentages than those from SPY, UDOW, and SPXL, should consider adding TSM and NVDA to thist that you track.

Comments

Post a Comment