Can Leveraged ETFs Safely Grow

Long-Term Investments?

This post compares the performance of five pairs of

ETFs. Within each pair is an unleveraged

ETF and a leveraged ETF based on five different market indexes. Read on to learn if leveraged ETFs consistently

outperformed unleveraged ETFs in the long run.

The ETFs are compared over three different timeframes: since

the ETF initially started trading (its launch date), over the last five years

of trading, and over the next to last five years of trading. By long-term investment, this post means

buying-and-holding an ETF for a period

of several years or decades – not just a couple of weeks, days, or minutes within a day. The first of the three timeframes begins with

the launch date for an ETF. Because

different ETFs can have different launch dates, the first timeframe can start on

different trading dates for different ETFs.

ETFs are compared in this post via their overall percentage

change and compound annual growth rate (cagr) for each of the three

timeframes. When the overall percentage

change is positive, then the ETF safely grows the assets allocated to a

long-term investment; that is, there is no loss of capital. The larger the cagr value is for an ETF, the

greater the compound annual growth is for the assets allocated to a long-term

investment. The greater the tendency for

an asset to grow from one year to the next, the greater the likely cagr for an asset

over a timeframe. This post also

compares leveraged ETFs to the SPY for those who seek a benchmark perspective

of the results.

The following table lists the five pairs of unleveraged and

leveraged ETFs tracked in this post along with the underlying market index for

each pair of ETFs. The reason for using

five different underlying market indexes is to capture results for different

types of security assets.

A Quick Introduction to ETFs and Market Indexes

An ETF is an investment fund that trades like a stock, bond,

or commodity on a market exchange. An

investment fund typically tracks other securities, such as a collection of the

top 500 stocks on the US stock exchanges (S&P 500 index). ETFs can be bought and sold at any time

during a trading day.

Mutual funds, which are early predecessors of ETFs, are also

investment funds that do not trade on market exchanges. Mutual funds are bought and sold from the

company sponsoring the investment fund.

Mutual fund firms allow investment fund shares to be bought and sold at

the end of a trading day based on its net asset value at that time.

The SPY AND SPXL tickers denote two different ETFs. The SPY is an unleveraged ETF based on the

S&P 500 index. When the S&P 500

index falls in price by one percent from the close of trading on the previous trading

day, then the SPY also falls by one percent at the time of purchase on the

current trading day. Similarly, if the S&P

500 index goes up by one percent from the close on the previous trading day,

then the SPY also goes up by one percent on that same day.

The SPXL ticker denotes a triple leveraged ETF. The price of the SPXL ticker also rises and

falls based on its underlying index, which is the S&P 500 index – just as

for the SPY ETF. However, the SPXL ETF

is leveraged by a factor of three. If

the price falls by 2 percent from the close of the previous trading day as of when

an SPXL share is purchased, the purchase price is 94% of the close price on the

previous trading day. Similarly, if the

price rises by 2 percent from the close of the previous trading day, the

purchase price rises by 6 percent from the close of the previous trading day. The leverage factor of three combined with

compounding over successive trading days can cause the price of the leveraged SPXL

ETF to change much more rapidly over several trading days than the unleveraged

SPY ETF.

Most market indexes are based on the weighted average of the

capital for the individual stocks in an index.

Market capital is defined as the product of share price times the total

number of outstanding shares. This

weighting by market capitalization can cause price changes for a few stocks in

an index to disproportionally impact the overall index value. The S&P 500 index is a market

capitalization weighted index.

There are other types of weighting schemes for indexes. For example, the DOW Industrial Average index

weights each stock component by its price instead of its market capitalization.

An Overview of Selected Data for this Post

The following screenshot shows an excerpt from SQL Server

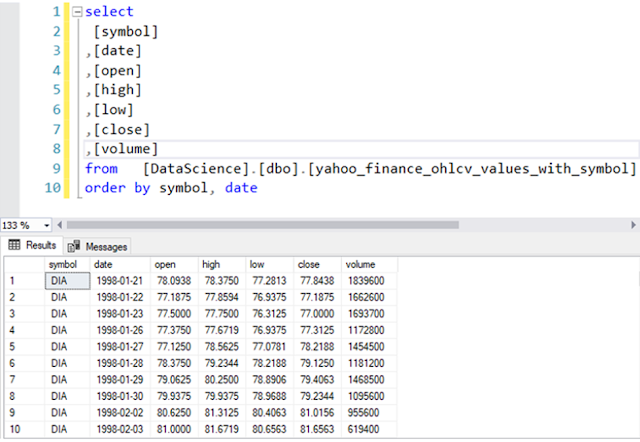

Management Studio. The top panel

contains a T-SQL script. The bottom

panel displays the first ten rows of the results set from script in the top

panel. The yahoo_finance_ohlcv_values_with_symbol

table is populated with historical price and volume data from the Yahoo Finance site for the ten

tickers tracked in this post.

The order by clause in the script sorts the results set rows

by trading dates within ticker symbols.

The displayed results are for the DIA ETF, and the launch date for the

DIA ticker symbol is 1998-01-21.

The next screenshot displays the last rows in the results set from the preceding script. As you can see, these rows are all for the UDOW ETF. The column to the left of the symbol column contains the row number. The last row in the results set has a date of 2023-12-29.

The last screenshot of this section displays some overall summary

data for each of the ten tickers tracked in this post.

- The first three columns are for the ticker symbol, the begin date, and the end date for each ETF.

o

The end date, 2023-12-29, is the same for all

ten tickers. This date is the final date

through which historical data are collected.

o

The begin date can vary by ticker. This is because the begin date reflects the

first trading date for which Yahoo Finance has historical trading data for a

ticker symbol.

- The last two columns reflect the total count of trading days from the begin date through the end date for each ticker as well as the fractional number to trading years for each ticker.

o

The count of trading days for each ticker is

merely the count of rows in the yahoo_finance_ohlcv_values_with_symbol table grouped

by ticker symbol.

o

According to Wikipedia,

there are an average of 252 trading days per calendar year. Therefore, the Fractional Trading Years column

values are the count of trading days for each ticker divided by 252.

The Comparison of ETF Tickers for All Tracked Trading Days

This post section shows the outcome of computing two metrics

to assess if leveraged ETFs can safely grow long-term investments more than unleveraged

ETFs. The results reported in this section

are for all trading days from the begin date through the end date for all five

pairs of tickers. These tickers are

specifically for ETFs based on market indexes, such as the S&P 500 index. The results may not apply to other ETFs that

track commodities, bonds, or single-stock ETFs (such as FBL or GGLL).

The first metric is the overall percent change of the close

price. You can compute this metric as

the close price on the end date less the close price on the begin date divided

by the close price on the begin date. If

this change percent is positive for a leveraged ETF, then the ETF can grow a

long-term investment safely. Otherwise,

the leveraged ETF does not grow long-term investment safely.

The second metric is the cagr, which assesses the average

percentage change on an annual basis from a begin date through an end date. The computational steps for computing this

metric are described and demonstrated in a prior

post. The code for the current post illustrates

how to perform the calculation in SQL Server with T-SQL code instead of with an

Excel spreadsheet.

Both metrics for each ticker symbol are computed from a

begin date through an end date designated, respectively, in the second and

third columns. The begin date is the first

trading date for which Yahoo Finance has historical price data for a ticker. The end date is the last trading date in 2023. Therefore, the metrics are computed over the

full lifetime of each ticker through the end of 2023.

Here’s a results set generated from a T-SQL script that computes

the comparison metrics for each ETF ticker.

The three most important columns are the first, next to last, and last

columns from the results set below.

·

The first column with a heading of symbol displays

the tickers for the ETFs tracked in this post.

·

The next to the last column has a header of

cagr. The more positive the value in

this column, the greater the average annual growth rate from the begin date

through the end date.

·

The last column has a column header of overall_percent_change. If the row value in this column is positive,

then the symbol for the ETF in the first column safely grows the capital invested

in it.

While the results set has all the information for comparing the

unleveraged versus the leveraged ETFs, it is not arranged in a format that

makes it easy to compare the two types of ETFs in terms of the comparison

metrics. Therefore, the results are

copied from the Results tab in SQL Server Management Studio to an Excel spreadsheet

that appears below.

Both the unleveraged and leveraged ETFs have positive overall percent change values, but the leveraged percent change values are substantially higher. The overall percent change values range from several hundred to more than eleven thousand. These values are quite large, but they describe change over a range of trading dates from about 14 years through about 30 years depending on when trade data became initially available for a ticker. It is also true that the cagr values for the leveraged ETFs are greater than for the unleveraged ETFs. Additionally, the leveraged cagr values exceed the unleveraged cagr values by a greater factor than is the case for the overall percent change metric. The cagr values for leveraged ETFs are generally about 3 to 4 times greater than the cagr values for unleveraged ETFs. Also, the leveraged ETF cagr values substantially exceed the cagr value for the SPY ticker, which denotes an unleveraged ETF. Because the cagr for the SPY ETF serves as a common benchmark for good market performance, this outcome confirms that a simple buy-and-hold strategy for leveraged market-based ETFs yield outstanding performance over the last 14 to 30 years.

|

For All Years |

||||||

|

Ticker |

Unleveraged |

Ticker |

Leveraged |

|||

|

CAGR |

Overall Percent Change |

CAGR |

Overall Percent Change |

|||

|

DIA |

6.28 |

384.14 |

UDOW |

25.19 |

2155.59 |

|

|

SPY |

7.99 |

974.15 |

SPXL |

24.89 |

2788.61 |

|

|

QQQ |

8.75 |

698.09 |

TQQQ |

40.94 |

11573.96 |

|

|

SOXX |

9.97 |

741.76 |

SOXL |

32.56 |

4774.26 |

|

|

IWM |

6.32 |

323.38 |

TNA |

15.00 |

724.45 |

|

The Comparison of ETF Tickers Over Two Successive Five-year Timeframes

Recall that the cagr computes compound annual growth rate

over a timeframe – from a begin date through an end date. Therefore, if the timeframe changes, you

would expect the cagr values to change.

The following display shows cagr values and overall percent

change for two different timeframes.

· The top table shows results for

the last five years of available trading data.

This is the timeframe from the first trading date in 2019 through the

last trading date in 2023.

· The bottom table shows results for the next to the last five years of available data. This is the timeframe from the first trading date in 2014 through the last trading date in 2018. These two timeframes have identical durations, but they extend over different date ranges. Therefore, the results by ticker are more comparable than the results for all years because each ticker in the preceding table can occur over a different timeframe.

Except for the IWM ticker which is based on the Russell 2000

index, the leveraged ETFs have consistently positive and larger overall growth

than for the unleveraged ETFs. In addition,

for the last 5 years table, the TNA ticker, which is for a leveraged ETF,

returned a negative cagr value while the IWM ticker, which is for a comparable

unleveraged ETF, returned a positive cagr value. In other words, leverage hurts the growth

rate for the TNA ETF in comparison to its matching unleveraged ETF (IWM).

While the remaining four pairs of ETFs (DIA and UDOW, SPY

and SPXL, QQQ and TQQQ, SOXX and SOXL) have a consistent trend of leveraged

ETFs returning superior cagr values, the cagr values are not identical for all

years versus either of the two fixed-duration timeframes. This implies, perhaps unsurprisingly, that growth

rates vary across timeframes even if there is a consistent tendency for

leveraged ETFs to return higher cagr values than for unleveraged ETFs.

Finally, it is worth mentioning that in both the last 5 year timeframe and next to the last 5 year timeframe, the leveraged ETFs returned consistently superior cagr values to the SPY. Because the SPY is a widely referenced security investment benchmark, these results indicate it may be possible to use leveraged ETFs as part of a strategy to generate substantially superior growth than the industry benchmark from the SPY ticker.

|

For Last 5 Years |

||||||

|

Ticker |

Unleveraged |

Ticker |

Leveraged |

|||

|

CAGR |

Overall Percent Change |

CAGR |

Overall Percent Change |

|||

|

DIA |

10.08 |

61.50 |

UDOW |

15.81 |

108.06 |

|

|

SPY |

13.73 |

89.99 |

SPXL |

25.92 |

215.79 |

|

|

QQQ |

21.51 |

164.41 |

TQQQ |

40.20 |

439.79 |

|

|

SOXX |

29.61 |

264.80 |

SOXL |

40.76 |

450.68 |

|

|

IWM |

8.33 |

29.05 |

TNA |

-1.63 |

-7.87 |

|

For Next-to-last 5 Years | ||||||

Ticker | Unleveraged | Ticker | Leveraged | |||

CAGR | Overall Percent Change | CAGR | Overall Percent Change | |||

DIA | 7.30 | 42.10 | UDOW | 20.98 | 158.72 | |

SPY | 6.45 | 36.63 | SPXL | 16.26 | 112.12 | |

QQQ | 12.09 | 76.76 | TQQQ | 29.74 | 266.70 | |

SOXX | 16.99 | 118.81 | SOXL | 38.37 | 405.57 | |

IWM | 3.26 | 17.34 | TNA | 2.38 | 12.43 | |

Summary

I hope you find these results of interest. For self-directed traders who manage their

own long-term investments, these analyses suggest an easy way (buy and hold) of

managing long-term investments --

presuming the market always goes up in the long run. For professional security advisors, these outcomes

offer, except for those based on the Russell 2000 index, historical guideposts

for beating industry benchmarks by substantial margins.

If you would like the programming files referenced in this

tip, please send a request to RickDobsonBlogs@gmail.com. These files do not include the historical

data because they belong to Yahoo Finance.

However, you can download historical data from Yahoo Finance for your

own custom analyses without charge. A

future post will provide readers of the Security Trading Analytics blog

detailed examples of how to download historical price and volume data from

Yahoo Finance.

I just recently started to blog, and I welcome your

suggestions about how to improve posts for you and the best ways to send files

from future posts to you. Thank you very much for any feedback that you

send to me.

Comments

Post a Comment